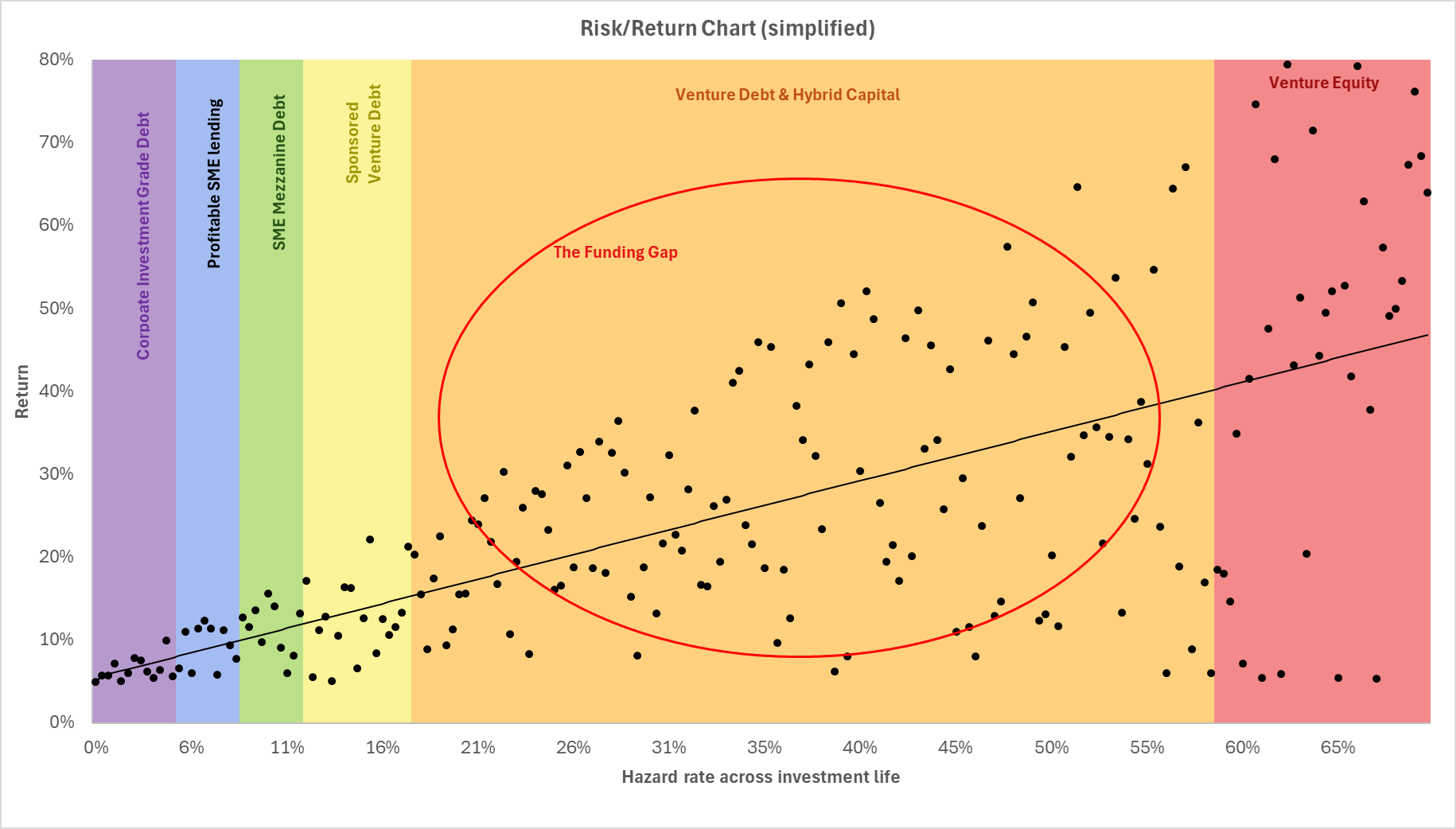

The Funding Gap

Why crossing the chasm from early adopters to mass adoption is so hard for European start-ups - and the role venture debt can play at Series A/B.

Crossing the chasm

In his seminal book, Crossing the Chasm, Geoffrey Moore explores how products that have strong appeal with early-stage adopters often fail to "cross the chasm" to mass adoption.

The book is a fascinating read, packed with real-life examples. While it was initially written as a marketing guide for products, it quickly became a bible for start-ups entering scale-up mode, as it clearly explains why promising companies fail. Success at the early stages doesn’t guarantee success later, especially when the needs of mainstream customers - and the demands of scaling - differ so radically from those of early adopters.

But as anyone who’s built a company knows, crossing the chasm isn’t just about the product. It’s about assembling a world-class team and, just as critically, securing the right funding to support growth. That’s where venture debt can play a game-changing role, especially at the Series A/B stage, where traditional funding options often fall short.

Series A & B: The hardest steps

In the UK, several schemes encourage angel investment in start-ups, such as the Enterprise Investment Scheme (EIS). These initiatives often involve generous tax offsets for losses. Alongside government incentives like R&D Tax Credits and Innovate UK grants, these measures have created a vibrant start-up scene.

The real test comes at Series A. By this stage, start-ups have typically outgrown these schemes, either because they’ve raised too much capital or achieved too much revenue to qualify. This transition is notoriously difficult, as companies must convince institutional investors they’re ready to scale while simultaneously proving operational resilience.

Adding to the challenge, Series A and B funding is the most dilutive for founders. Institutional investors demand significant equity in exchange for their capital, leaving founders with reduced ownership of the business they’ve worked so hard to build.

What about debt?

As mentioned in our previous blog post, Europe’s venture equity capital market is far smaller than that of the US: the top five VC funds in Europe combined are smaller than the smallest of the top five US players. This of course exacerbates the dilution problem so founders often turn to debt as an alternative, or complementary solution.

Unfortunately, the funding situation is even more dire when it comes to debt, as the comparison between European and US markets highlights.

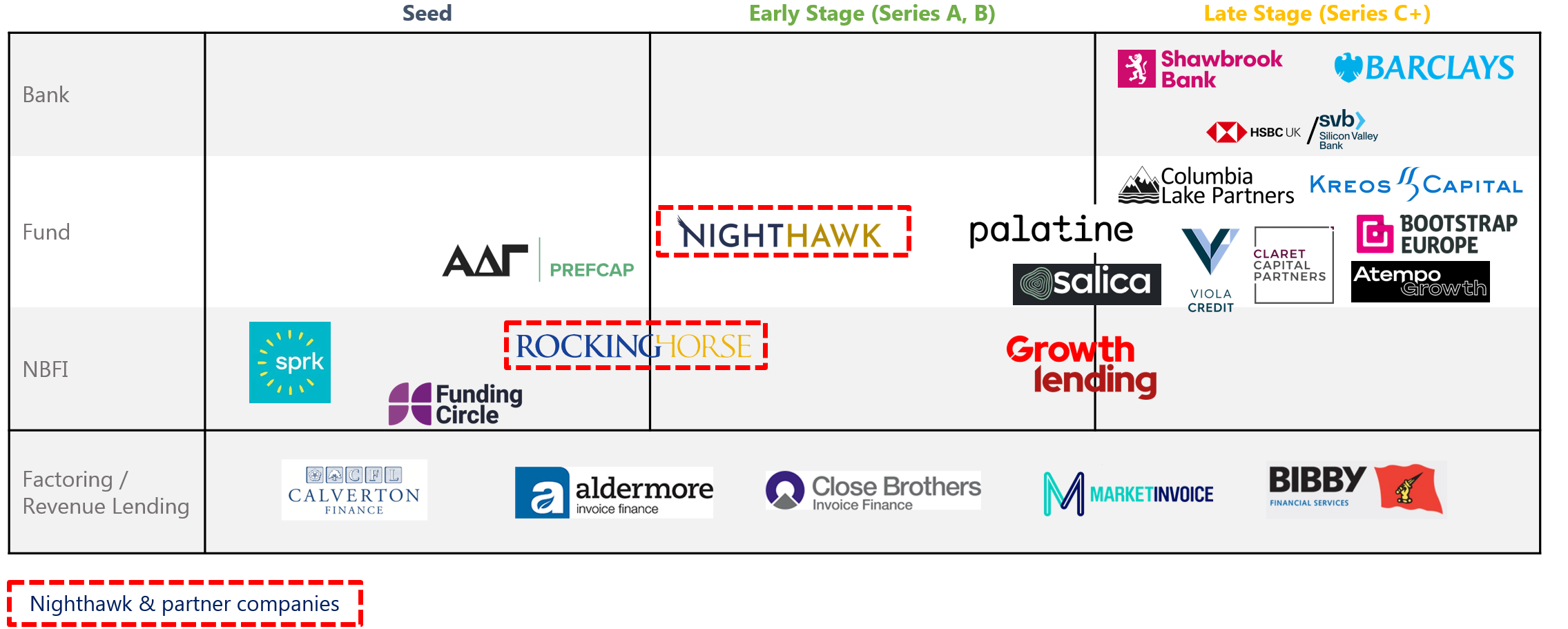

The European venture debt scene

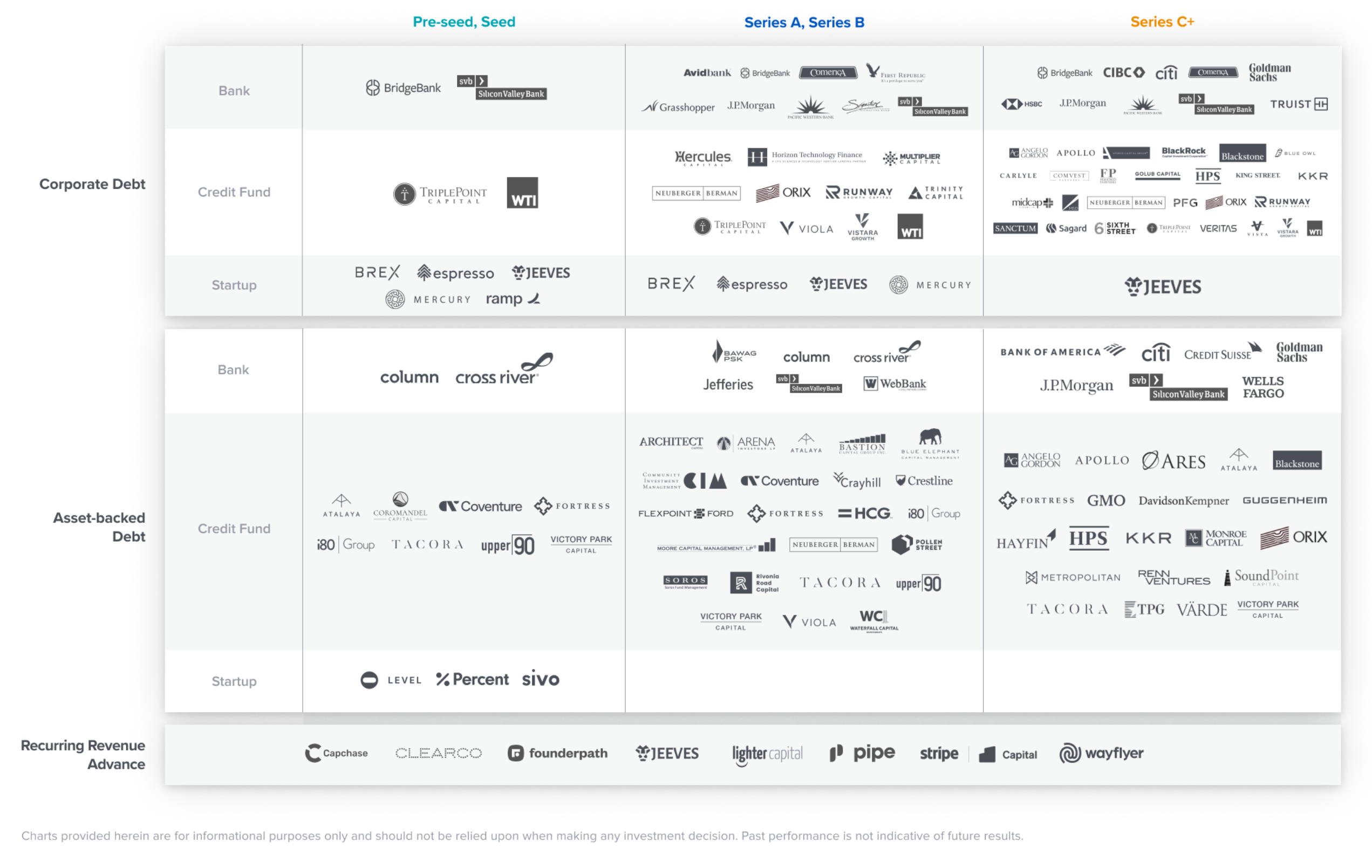

The US venture debt scene

Source: Andreessen Horowitz - 16 Things to Know About Raising Debt for Startups.

The early-stage debt gap

Whilst the comparison above demonstrates the lack of debt funding, particularly at the early stage, it does not explain why this gap exists. At a high level, the answer is simple: venture debt is still new to the European markets, and Europeans have a lower risk tolerance.

The pronounced early-stage gap is more complex to explain. Early-stage companies are perceived as riskier overall because:

- Sponsors, if present, are less deeply embedded and more likely to write off their investments.

- Customers face lower switching costs, making revenue streams less predictable.

- Team structures and leadership stability remain uncertain.

Debt-equity hybrid

Given these risks, lenders need the skills of both equity and debt investors:

- they need a deep understanding of the business itself, its growth potential and valuation, just as venture capitalists do, but

- they need to balance this assessment with the more limited upside inherent to debt investments.

This gap is great news for investors: a market where there is both a lack of available capital and a lack of skill usually results in excellent returns for a sustained period; private equity and hedge funds were great examples of this.

What about founders? Early-stage venture debt is more expensive than the equivalent at Series C. However, since Series A/B are the most dilutive, taking debt earlier remains extremely attractive.

In a transaction closed this year, our debt gave our client an extra 6 months of runway, enabling them to complete their Series B at 50% higher valuation than initially discussed with investors. In this context, paying another few percentage points on a small amount of debt is totally immaterial.

In conclusion

Crossing the chasm from early adoption to mass adoption remains one of the most significant challenges for start-ups. While product scalability and team building are critical, securing the right funding is equally essential - and venture debt should be part of that equation for founders. For investors, venture debt remains extremely attractive given the supply/demand imbalance.