Farewell SVB, you will be missed

With First Citizens taking over SVB's US assets and HSBC the UK ones, was SVB's business model fundamentally broken? A look at the balance sheet.

With First Citizens bank taking over the US assets of SVB in the United States, and HSBC having taken over the UK assets, Silicon Valley Bank has now disappeared for good.

So, with unmistakeable nostalgia, we are going to try to answer a simple question here: was SVB's business model fundamentally broken?

1. Low cost of funding has a cost

I have to admit, I didn't look at SVB's balance sheet until 2023. As a competitor we saw them quite often, and my impression was that their credit process was pretty decent. What we did see was that SVB was generally more aggressive than us on pricing - largely driven by a very low cost of funding we could not match.

That's a cost of funding of 0.57%: lower than the US government. However, the low percentage of SVB insured deposits (less than 3%) seems to have precipitated the run on the bank, so relying on such cheap uninsured deposits certainly is not without downside risks.

2. Trigger - the HTM losses

The trigger for the run on the bank was the rights issue they had to organise in order to plug a hole in the sale of their hold-to-maturity losses. The fact the HTM losses were more than 100% of their core tier-1 capital put them in a particularly bad spot, but others have done this. SVB's particular crime seems to have been to be reliant on a small ecosystem.

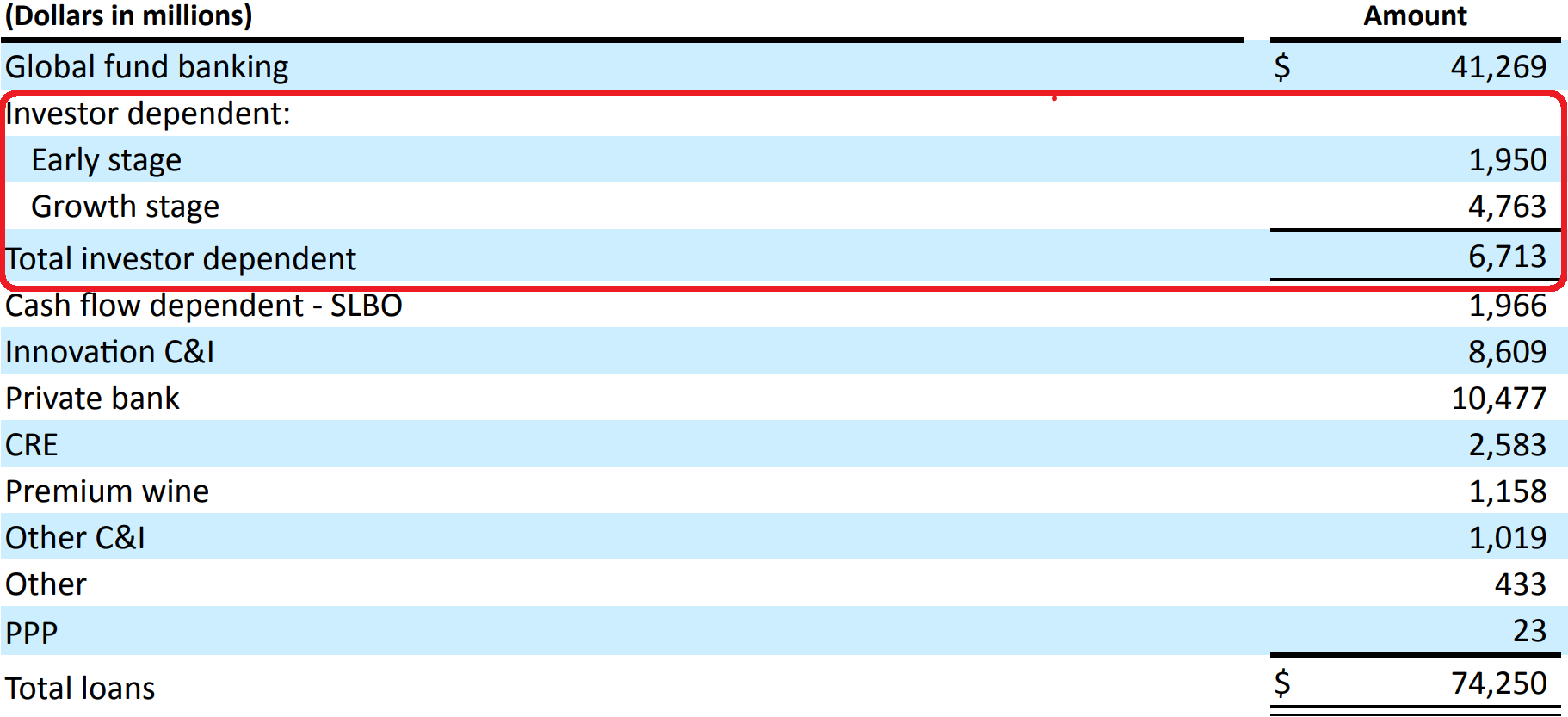

3. SVB's assets

The SVB loan book was barely 40% of its balance sheet. It had grown deposits at a rate that exceeded its ability to make loans. Even more surprising, its venture debt book - the area we saw them most - was in fact tiny.

$6.7bn Venture Debt book (Investor Dependent - Early Stage and Growth Stage in SVB terminology). That's 9% of the loan book, or barely 3% of the overall balance sheet.

4. Overall a good book

These certainly aren't the kind of losses that have anyone going on a bank run; whilst it no doubt had some issues, it certainly does not seem to point to a "fundamentally broken business model".

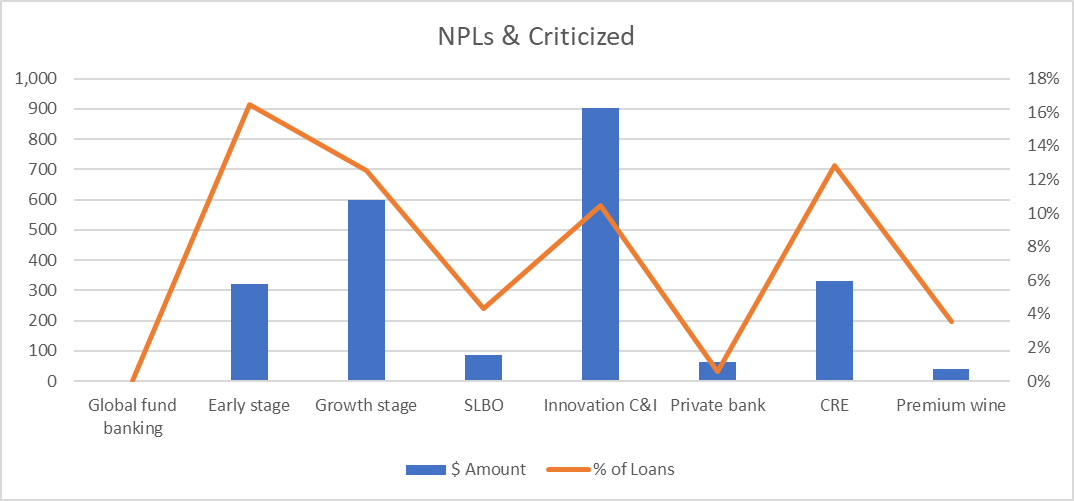

5. Issues concentrated in 4 areas

The issues were concentrated in its Innovation C&I book, CRE and venture debt. The Global Fund Banking book was impressively resilient.

6. Worsening venture debt quality

Whilst overall the loan book was healthy, the venture debt book was showing cracks, with Early-Stage debt in particular difficulty: over 15% of loans were past-due. Not surprising given the state of the tech markets in 2022.

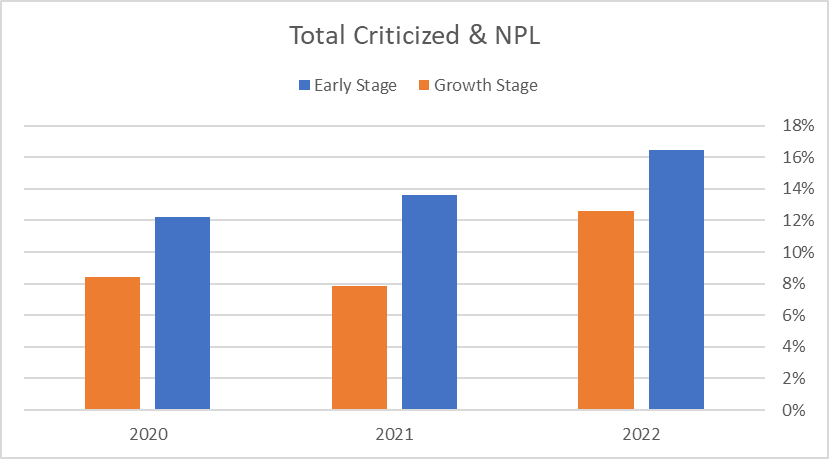

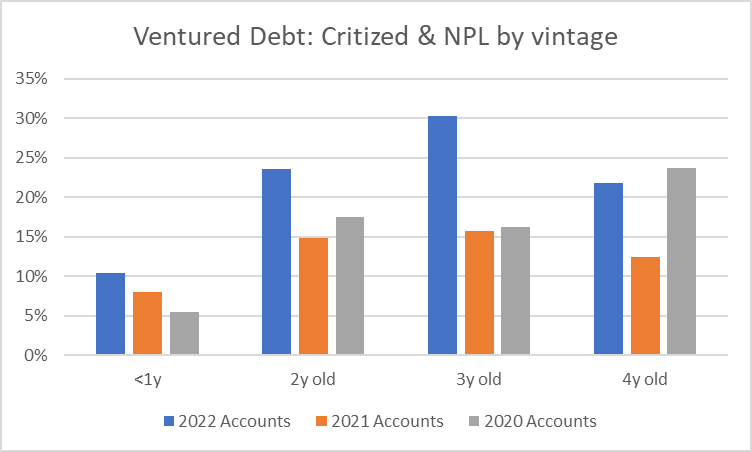

7. Some extend & pretend

Older loans show significant deterioration - the amount of criticized & NPL loans over 2 years old is nearly double what they were historically. At fair value, this probably means at least a 10% impairment for venture debt loans of 2y or more - i.e. at least $200mm. Given the prices First Citizens and HSBC paid for SVB, these costs are easily absorbable. Both HSBC and First Citizens have made great deals.

Conclusion

So was SVB's business model fundamentally broken?

- In its over-reliance on cheap deposits from a single sector, yes

- In its amateurish handling of treasury matters, yes

- In its loan book overall, no - but there were areas of stress

- In its venture debt book, no, but there were significant stresses, and it was almost certainly under-pricing the risk

The mispricing of the loan book risk may well have been a significant contributor to the bankruptcy of SVB. This leaves us with an open question: will the buyers of the SVB book continue to provide credit to the tech ecosystem?