The rare case of helping investors and start up founders.

Why founders are better off complementing venture capital with venture debt and R&D financing at the early stages - and why this also works for investors.

The traditional view is that venture capital helps early stage companies with debt funding used once the company is profitable. The argument goes along the lines that:

- For the investor: the risks of an early stage company are high, hence equity risk is uncapped, whilst debt with warrants is capped. Why bother with debt at the early stages of a company, since they both share similar risks of default? We show this is not the case.

- For the founder: equity is permanent capital that does not need any return for a protracted period of time, whilst debt needs to be repaid, often with fresh equity capital. We argue this is not the case with Innovate UK and R&D loans.

With the help of Carta's publicly disclosed data from Peter Walker, we argue that founders are better off complementing their venture capital injections with venture debt and R&D financing at the early stages of their journey.

The case for the founder

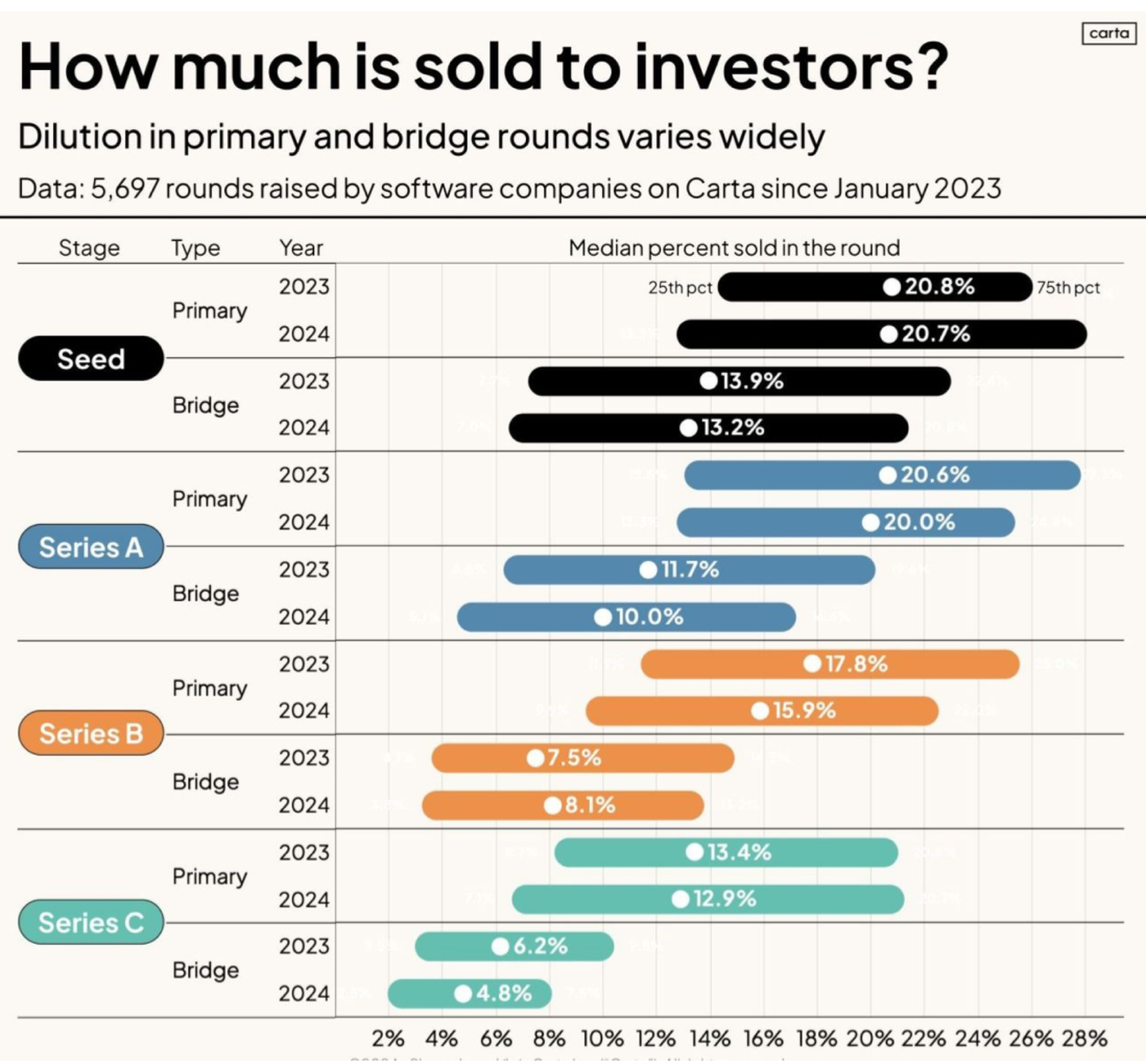

The chart below shows the average dilution by equity rounds in SaaS companies in the US, according to Carta. On average, a founder could be diluted by 70% by the time their company breaks even (Series C), assuming they only do primary rounds. If they have to do bridge rounds, the dilution is prohibitive.

Source: Carta.

The most dilutive capital raising rounds are the early stage ones. We argue that Innovate UK grants combined with R&D loans can limit dilution by avoiding the seed/bridge component of the fund raise, saving 13%–40% dilution.

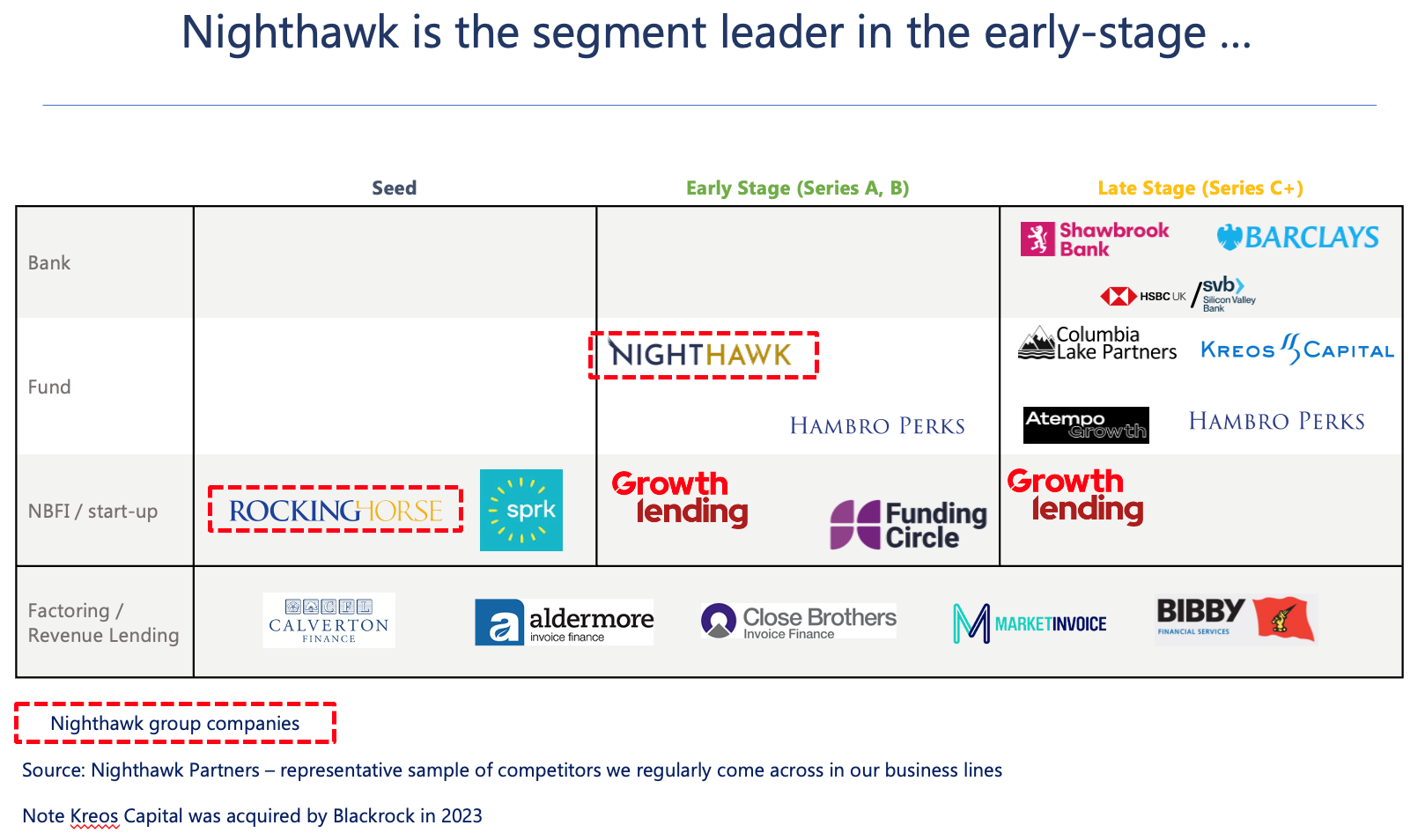

- Up to Series B, lending against Innovate UK and R&D grants is best.

- Venture debt can really kick in from Series A or, more realistically, Series B, as it is a longer-duration loan that requires £2mn of revenues and expects larger orders over a 12–18 month period.

- At Series B, export finance also fits - requiring established revenues including international ones.

Source: Nighthawk Partners.

The case for the investor

For the right business, R&D financing and venture debt can materially increase the stake the founder has when they exit. Most investors believe early-stage equity is better than debt. We disagree.

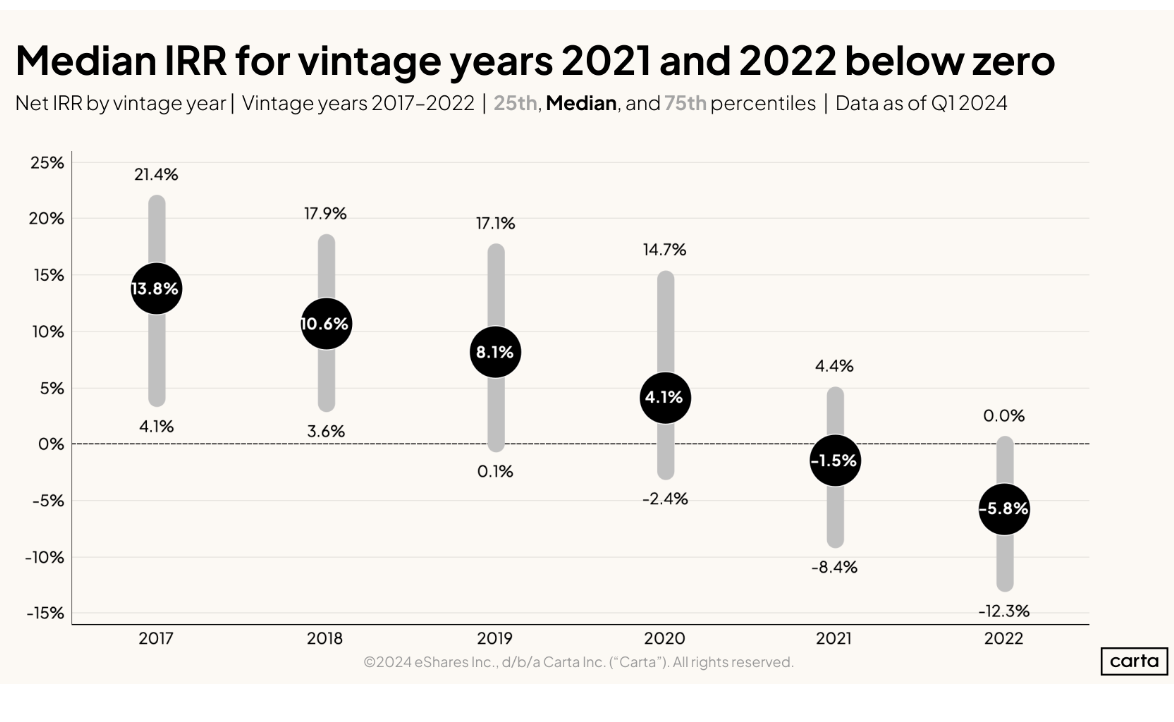

On a single successful company, equity is better than debt. However, most VCs invest in a portfolio. Considering the high default rates of these companies over a seven-year period, IRRs are close to 12%. In R&D lending and venture debt, portfolio returns have averaged 15%+ over the past 5 years, through a combination of finite investment period, warrants and senior capital position in case of default. As a result, these forms of debt, at portfolio level, produce better returns than the riskier equity venture capital firms - potentially offering better risk/reward up to Series B, with equity investments made as visibility on the business improves.

Source: Carta.