Drop The Sponsor

Most venture debt relies on a VC "sponsor". At Nighthawk we prefer unsponsored loans - and they are a better deal for both founders and investors.

Executive Summary

Most of the venture debt industry relies on "sponsors" when making loans - a VC firm that has invested heavily in the borrower and provides lenders with confidence in the business's prospects.

At Nighthawk, we collaborate with several VCs and appreciate seeing them on the cap table. However, we do not rely on them to sponsor deals - in fact, we prefer making "unsponsored" loans. Our lending decisions are fully independent and do not need to be tied to an equity raise.

As we discuss below, this approach offers a better deal for both founders and our investors.

Avoiding Dilution

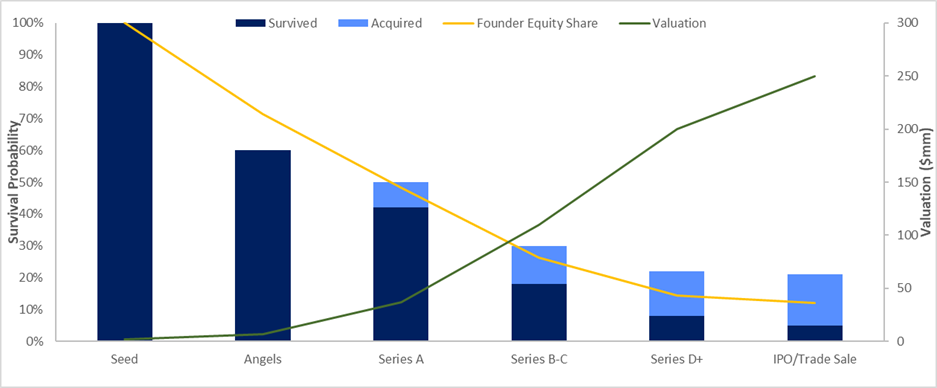

Taking a step back, the main issue successful founders face is dilution. As you can see below, the average founder owns just 12% of their business by the time they exit.

Venture debt has become an increasingly important tool to combat dilution. In the U.S., companies like Google, Facebook, Uber, Airbnb, and Dropbox all used it early on. We are now seeing European founders follow suit.

Extending the runway

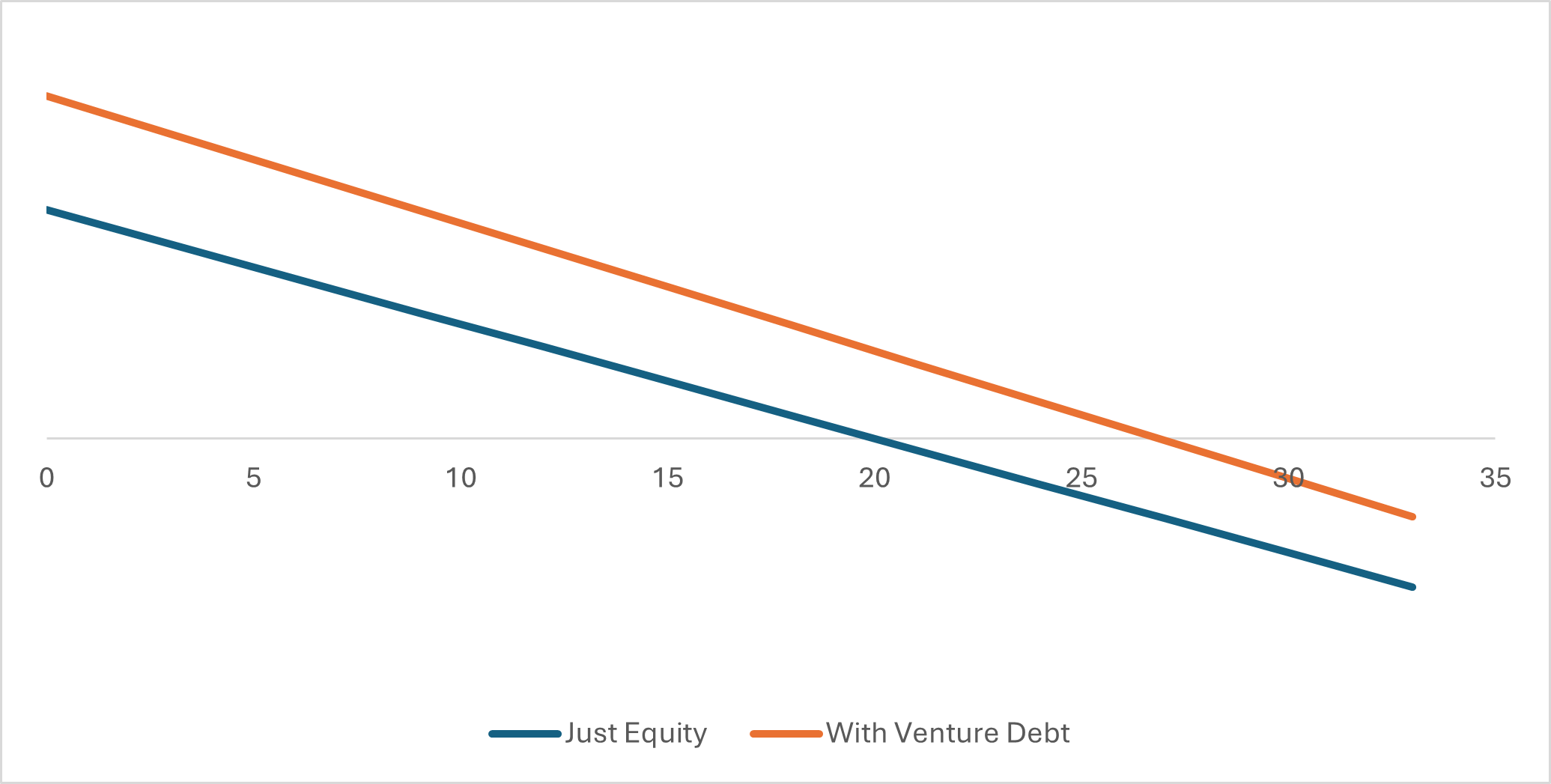

Venture debt aims to extend a company’s cash runway. Let's look at DailySaaS, a theoretical example of a typical sponsored debt issuance:

- £2mm equity raised with Big VC (the sponsor)

- cash burn of £100k/month

- Runway before debt: 20 months

- Venture debt offer: £1M, 5-year term, 14% interest

As the chart shows: venture debt adds seven months of runway, but DailySaaS pays interest for the full 20 months before needing the cash. The effective interest cost over those seven months is therefore 54% - far higher than it appears at first glance.

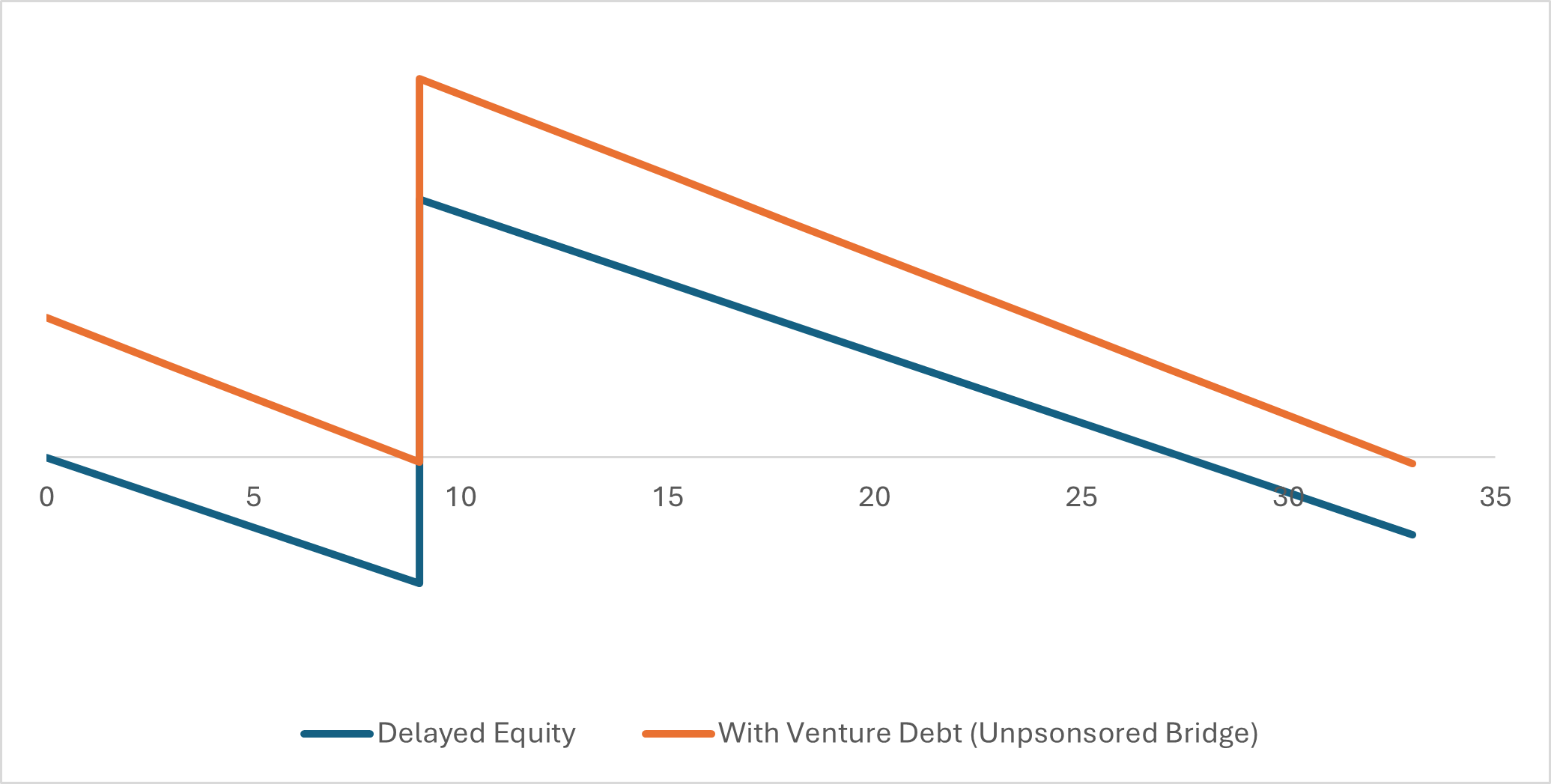

A Smarter Approach to Venture Debt

A better solution is to raise the debt when you need it - e.g. ahead of an equity raise to extend the cash runway. This significantly increases the runway of the company, thanks in part to the higher valuation that can be reached on the equity raise by delaying it.

The flip side is a slightly higher interest rate (typically around 18%), but:

- Interest payments only begin when the company actually needs the capital.

- Once equity is raised, the debt starts amortizing, reducing long-term costs.

- Early repayment is often possible with reasonable fees.

As a result, the lifetime cost of unsponsored debt can be half that of sponsored debt.

A Better Deal for Investors Also

So why is this a better deal for debt investors too?

1. Higher Returns - Unsponsored debt commands higher interest rates and/or more favourable warrants.

2. Safer Repayments - Unsponsored debt usually has stricter break-even target requirements, meaning the companies are usually better credits. The unsponsored lender also has a clear understanding of when and from whom the borrower will raise in the next 6–12 months. In contrast, sponsored deals rely on companies finding investors in 4–5 years.

3. Eliminating Conflicts of Interest - Sponsored lenders rely on VCs to bring them deals: how willing would they be to force a down round if needed? Some venture debt providers also have VC arms, creating misaligned incentives. Unsponsored lenders, being fully independent, avoid this issue.

4. Better Warrant Terms - Who gets better warrant terms: the lender reliant on VCs for deals, or the lender working directly with founders?

5. Stronger Portfolio Selection - VCs introduce venture lenders to their bottom 80%, not their top 20%. A venture debt lender aligned with founders can select the best deals from the entire market rather than being limited to a VC’s weaker bets.

In summary

Whether you’re a founder or an asset allocator, unsponsored venture debt offers a far better deal. Get the funding and returns you need - on your terms.